Fueling Your Dream: Navigating the World of the Small Business Loan

Every great business starts with an idea, passion, and relentless hard work. But often, turning that vision into a thriving reality requires something more tangible: capital. Whether you’re launching a startup, expanding your operations, navigating seasonal cash flow, or investing in critical equipment, funding is the lifeblood that keeps businesses moving forward. For countless entrepreneurs, the answer lies in securing a small business loan.

- What Exactly is a Small Business Loan?

- Why Do Businesses Seek a Small Business Loan?

- Exploring the Different Types of Small Business Loans

- Demystifying the Small Business Loan Application Process

- What Lenders Look For: The 5 C’s of Credit

- Improving Your Chances of Small Business Loan Approval

- Alternatives to a Traditional Small Business Loan

- Spotlight on Rancho Cucamonga: Opportunities for Investors & Businesses

- Partnering for Success: Why Consider GHC Funding?

- Conclusion: Taking the Next Step Towards Funding Your Vision

- What Exactly is a Small Business Loan?

- Why Do Businesses Seek a Small Business Loan?

- Exploring the Different Types of Small Business Loans

- Demystifying the Small Business Loan Application Process

- What Lenders Look For: The 5 C's of Credit

- Improving Your Chances of Small Business Loan Approval

- Alternatives to a Traditional Small Business Loan

- Spotlight on Rancho Cucamonga: Opportunities for Investors & Businesses

- Partnering for Success: Why Consider GHC Funding?

- Conclusion: Taking the Next Step Towards Funding Your Vision

Navigating the landscape of business financing can seem daunting. With various loan types, eligibility requirements, and application processes, knowing where to start is often the biggest hurdle. This comprehensive guide is designed to demystify the small business loan, equipping you with the knowledge to confidently seek the funding your business needs to succeed.

We’ll cover everything from the fundamental definition and common uses of a small business loan to the different types available, the step-by-step application process, and what lenders look for. We’ll also touch upon alternatives and provide specific resources for entrepreneurs and investors, particularly those eyeing opportunities in the dynamic market of Rancho Cucamonga, California. For businesses seeking tailored financing solutions, including commercial real estate (CRE) and general business loans, partners like GHC Funding specialize in helping businesses access the capital they need.

Need capital? GHC Funding offers flexible funding solutions to support your business growth or real estate projects. Discover fast, reliable financing options today!

⚡ Key Flexible Funding Options:

GHC Funding everages financing types that prioritize asset value and cash flow over lengthy financial history checks:

DSCR Rental Loan

- No tax returns required

- Qualify using rental income (DSCR-based)

- Fast closings ~3–4 weeks

SBA 7(a) Loan

- Lower down payments vs banks

- Long amortization improves cash flow

- Good if your business occupies 51%+

Bridge Loan

- Close quickly — move on opportunities

- Flexible underwriting

- Great for value-add or transitional assets

SBA 504 Loan

- Low fixed rates through CDC portion

- Great for construction, expansion, fixed assets

- Often lower down payment than bank loans

🌐 Learn More

For details on GHC Funding's specific products and to start an application, please visit our homepage:

Small Business Loan" class="wp-image-3438" srcset="https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-1024x1024.jpeg 1024w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-300x300.jpeg 300w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-150x150.jpeg 150w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-768x768.jpeg 768w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-1536x1536.jpeg 1536w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-1080x1080.jpeg 1080w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b.jpeg 2048w" sizes="(max-width: 1024px) 100vw, 1024px" />

Small Business Loan" class="wp-image-3438" srcset="https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-1024x1024.jpeg 1024w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-300x300.jpeg 300w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-150x150.jpeg 150w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-768x768.jpeg 768w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-1536x1536.jpeg 1536w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b-1080x1080.jpeg 1080w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_2k4b9d2k4b9d2k4b.jpeg 2048w" sizes="(max-width: 1024px) 100vw, 1024px" />What Exactly is a Small Business Loan?

At its core, a small business loan is a sum of money borrowed from a financial institution (like a bank, credit union, online lender, or specialized financing company) that a business owner agrees to pay back, plus interest and any associated fees, over a predetermined period.

Think of it as an investment in your business, provided by an external party. This capital injection can be used for a multitude of purposes, enabling businesses to overcome financial obstacles and seize growth opportunities they might otherwise miss. Unlike equity financing (where you sell a portion of your company ownership), a small business loan allows you to retain full ownership while accessing necessary funds.

Why Do Businesses Seek a Small Business Loan?

The reasons businesses need financing are as diverse as the businesses themselves. However, some common scenarios necessitate applying for a small business loan:

- Startup Costs: Launching a new venture involves significant upfront expenses – securing a location, purchasing initial inventory, marketing, hiring initial staff, obtaining licenses, and more. A startup small business loan can provide the foundational capital needed to get off the ground.

- Expansion and Growth: Ready to take your business to the next level? This might involve opening a new location, launching a new product line, entering new markets, or scaling up production. A small business loan can fund these ambitious growth initiatives.

- Working Capital: Day-to-day operational expenses (payroll, rent, utilities, inventory replenishment) require consistent cash flow. Sometimes, especially for seasonal businesses or during slow periods, gaps emerge. A working capital small business loan helps bridge these gaps, ensuring smooth operations.

- Equipment Purchases: Whether it’s upgrading technology, buying heavy machinery, acquiring new vehicles, or investing in specialized tools, equipment is often essential for efficiency and competitiveness. Equipment financing, a specific type of small business loan, is designed for these purchases.

- Inventory Management: Businesses, particularly in retail or manufacturing, need adequate stock to meet customer demand. A small business loan can help purchase inventory in bulk (potentially securing better pricing) or manage seasonal inventory fluctuations.

- Commercial Real Estate: Buying, renovating, or refinancing property for your business operations is a major investment. Commercial Real Estate (CRE) loans, a specialized form of business financing, make these significant purchases possible. Companies like GHC Funding offer dedicated CRE loan programs.

- Refinancing Existing Debt: Businesses might seek a new small business loan to consolidate existing debts or refinance a previous loan under more favorable terms (e.g., a lower interest rate or longer repayment period).

- Marketing and Advertising: Investing in strategic marketing campaigns can significantly boost brand awareness and customer acquisition, driving revenue growth.

- Hiring Staff: Expanding your team to support growth requires funding for salaries, benefits, and training.

Exploring the Different Types of Small Business Loans

Not all funding needs are the same, and thankfully, neither are the loan options. Understanding the various types of small business loans helps you choose the one that best aligns with your specific requirements:

- Term Loans:

- What it is: A lump sum of capital paid back in regular installments (usually monthly) over a set period (term), ranging from a few months to several years. Interest rates can be fixed or variable.

- Best for: Significant one-time investments like expansion projects, major equipment purchases, or acquisitions. Predictable repayment schedules make budgeting easier.

- SBA Loans (Small Business Administration):

- What it is: Loans partially guaranteed by the U.S. Small Business Administration but issued by traditional lenders (banks, credit unions). The government guarantee reduces risk for lenders, often resulting in more favorable terms (lower interest rates, longer repayment periods) for borrowers.

- Common Programs:

- SBA 7(a) Loan: The most common type, versatile for various purposes including working capital, expansion, and equipment.

- SBA 504 Loan: Primarily for purchasing major fixed assets like commercial real estate or heavy machinery. Requires owner contribution and involves a Certified Development Company (CDC).

- SBA Microloan: Smaller loan amounts (up to $50,000) often targeted at startups and underserved communities, typically provided through intermediary non-profit lenders.

- Best for: Businesses seeking favorable terms and longer repayment periods, though the application process can be more intensive.

- Business Lines of Credit:

- What it is: Provides access to a predetermined amount of capital that you can draw from as needed, up to the credit limit. You only pay interest on the amount you actually use. As you repay the drawn funds, the available credit replenishes (similar to a credit card).

- Best for: Managing cash flow fluctuations, unexpected expenses, short-term working capital needs, or seizing time-sensitive opportunities. Offers flexibility.

- Equipment Financing:

- What it is: A loan specifically used to purchase business equipment. The equipment itself typically serves as collateral for the loan.

- Best for: Acquiring machinery, vehicles, technology, or other essential business equipment without tying up working capital. Loan terms often match the expected lifespan of the equipment.

- Invoice Financing (or Factoring):

- What it is: Uses your outstanding customer invoices (accounts receivable) as collateral.

- Invoice Financing: You borrow money against your invoices.

- Invoice Factoring: You sell your invoices to a factoring company at a discount for immediate cash. The factor then collects payment from your customers.

- Best for: Businesses with long payment cycles (e.g., 30, 60, 90 days) that need cash sooner to cover operational costs.

- What it is: Uses your outstanding customer invoices (accounts receivable) as collateral.

- Merchant Cash Advances (MCAs):

- What it is: Not technically a loan, but an advance based on future credit/debit card sales. A lump sum is provided upfront, which is repaid through a fixed percentage of daily card sales, plus a fee (expressed as a factor rate, which can be very high).

- Best for: Businesses needing very fast funding with high daily card sales, but often comes with extremely high costs. Use with caution and understand the terms thoroughly.

- Commercial Real Estate (CRE) Loans:

- What it is: Specific financing designed for purchasing, developing, or refinancing properties used for business purposes (office buildings, retail spaces, industrial warehouses, etc.).

- Best for: Businesses looking to own their premises or invest in income-generating commercial property. Terms are typically longer than standard business loans. Specialized lenders like GHC Funding focus on these types of loans, understanding the nuances of property financing. Check out their business loan options, which often include CRE financing.

- Working Capital Loans:

- What it is: Short-term loans designed specifically to cover everyday operational expenses rather than long-term assets or investments.

- Best for: Bridging temporary cash flow gaps, funding payroll, purchasing short-term inventory. GHC Funding provides various business loan solutions that can address working capital needs.

Demystifying the Small Business Loan Application Process

While specifics vary by lender and loan type, the journey to securing a small business loan generally follows these steps:

- Assess Your Needs & Purpose: Clearly define why you need the loan and exactly how much capital is required. Lenders want to see a clear, justifiable purpose for the funds. Over-borrowing increases debt burden, while under-borrowing might not solve the problem.

- Check Your Eligibility: Before applying, evaluate your standing. Key factors include:

- Credit Score: Both personal and business credit scores are crucial. Higher scores generally lead to better terms.

- Time in Business: Many lenders prefer businesses operating for at least 1-2 years, though startups can find specific programs (like some SBA loans or microloans).

- Annual Revenue: Lenders need assurance that your business generates sufficient income to support loan repayment. Minimum revenue requirements vary.

- Industry: Some lenders specialize in or avoid certain industries.

- Gather Necessary Documentation: This is often the most time-consuming part. Be prepared to provide:

- Business Plan: Especially crucial for startups or significant expansion loans. Outlines your business model, market analysis, management team, and financial projections.

- Financial Statements: Balance sheets, income statements (profit & loss), cash flow statements (typically for the last 2-3 years, if applicable).

- Tax Returns: Personal and business tax returns (usually 2-3 years).

- Bank Statements: Business bank statements (several months).

- Legal Documents: Business licenses, permits, articles of incorporation/organization, franchise agreements (if applicable).

- Loan Application Form: The lender’s specific application document.

- Information on Collateral: If applying for a secured loan.

- Research and Select Lenders: Don’t just go with the first option. Compare different types of lenders:

- Traditional Banks: Often offer competitive rates but may have stricter requirements.

- Credit Unions: Similar to banks, potentially more community-focused.

- Online Lenders (FinTech): Typically offer faster processing and potentially more flexible requirements, but sometimes at higher rates.

- Specialized Lenders: Companies focusing on specific loan types, like GHC Funding for CRE and business loans, may offer deeper expertise.

- SBA-Approved Lenders: Required for SBA-guaranteed loans.

- Compare Loan Offers: Carefully evaluate offers based on:

- Annual Percentage Rate (APR): The true cost of borrowing, including interest rate and fees.

- Loan Term: The repayment period. Longer terms mean lower payments but more total interest paid.

- Fees: Origination fees, underwriting fees, prepayment penalties, late fees.

- Collateral Requirements: What assets (if any) you need to pledge.

- Repayment Schedule: Frequency and amount of payments.

- Submit Your Application: Ensure all information is accurate and complete. A well-prepared application package makes a strong impression.

- Underwriting and Approval: The lender reviews your application, financials, credit history, and supporting documents to assess risk and make a lending decision. They may ask follow-up questions.

- Funding: If approved, you’ll sign the loan agreement, and the funds will be disbursed according to the agreed terms.

What Lenders Look For: The 5 C’s of Credit

Lenders evaluate risk using a framework often called the “5 C’s of Credit.” Understanding these helps you strengthen your small business loan application:

- Character: Your track record and reputation. Lenders assess your personal and business credit history, experience in your industry, and overall trustworthiness. A history of responsible financial behavior is key.

- Capacity: Your ability to repay the loan. Lenders analyze your business’s cash flow, revenue streams, and existing debt obligations (Debt Service Coverage Ratio – DSCR) to determine if you can comfortably handle the loan payments.

- Capital: The amount of personal investment you (the owner) have put into the business. Lenders like to see that you have “skin in the game,” as it demonstrates commitment and confidence in the venture.

- Collateral: Assets pledged to secure the loan (e.g., real estate, equipment, inventory). If you default on the loan, the lender can seize the collateral to recoup their losses. Not all loans require collateral (unsecured loans), but secured loans often have lower interest rates.

- Conditions: The purpose of the small business loan, the amount requested, prevailing economic conditions, and the state of your industry. Lenders consider how these external factors might impact your business’s ability to succeed and repay the debt.

Improving Your Chances of Small Business Loan Approval

- Develop a Strong Business Plan: Clearly articulate your vision, strategy, market, and financial projections.

- Maintain Good Credit: Regularly monitor and work to improve both your personal and business credit scores. Pay bills on time and manage existing debt wisely.

- Keep Financials Organized: Have accurate, up-to-date financial statements readily available. Use accounting software or hire a professional.

- Offer Collateral (If Possible/Applicable): Securing the loan can significantly increase approval odds and potentially lower rates.

- Be Realistic About Funding Needs: Request an appropriate loan amount tied to a clear, well-justified purpose.

- Choose the Right Lender and Loan Type: Apply for loan products that match your needs and profile, and approach lenders whose criteria you likely meet. For specific needs like property acquisition, a specialist like GHC Funding might be a better fit than a generalist lender.

Small Business Loan" class="wp-image-3439" srcset="https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-1024x1024.jpeg 1024w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-300x300.jpeg 300w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-150x150.jpeg 150w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-768x768.jpeg 768w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-1536x1536.jpeg 1536w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-1080x1080.jpeg 1080w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6.jpeg 2048w" sizes="(max-width: 1024px) 100vw, 1024px" />

Small Business Loan" class="wp-image-3439" srcset="https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-1024x1024.jpeg 1024w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-300x300.jpeg 300w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-150x150.jpeg 150w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-768x768.jpeg 768w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-1536x1536.jpeg 1536w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6-1080x1080.jpeg 1080w, https://ghcfunding.com/wp-content/uploads/2024/08/Gemini_Generated_Image_kgt6wzkgt6wzkgt6.jpeg 2048w" sizes="(max-width: 1024px) 100vw, 1024px" />Alternatives to a Traditional Small Business Loan

If a traditional small business loan isn’t the right fit or you don’t qualify, consider these alternatives:

- Crowdfunding: Raising small amounts of money from many people, typically via online platforms (e.g., Kickstarter, Indiegogo for rewards-based; platforms like Fundable for equity).

- Angel Investors & Venture Capital (VC): High-growth potential businesses might attract investment from individuals (angels) or firms (VCs) in exchange for equity ownership. This is particularly relevant for tech startups and scalable businesses.

- Small Business Grants: Free money that doesn’t need repayment, but competition is fierce, and grants often target specific industries, demographics, or purposes. Check Grants.gov and specific industry/local programs.

- Personal Savings: Using your own funds avoids debt but puts personal assets at risk.

- Friends and Family Loans: Can be easier to obtain but potential to strain personal relationships if not structured professionally with clear repayment terms.

Spotlight on Rancho Cucamonga: Opportunities for Investors & Businesses

Rancho Cucamonga, strategically located in the Inland Empire region of Southern California, presents a compelling environment for both business owners and investors. Its proximity to major transportation corridors (I-10, I-15, Ontario International Airport), a growing and diverse population, a strong base in logistics and distribution, healthcare, retail, and education, make it an attractive hub.

For investors considering opportunities in Rancho Cucamonga, understanding the local economic landscape and accessing relevant resources is crucial. Businesses operating here or looking to relocate may also find specific advantages when seeking a small business loan or other forms of capital.

Helpful External Resources for Investors & Businesses in Rancho Cucamonga:

- City of Rancho Cucamonga Economic Development: Provides information on local business climate, development opportunities, demographics, and business assistance programs. A primary resource for anyone looking to invest or establish a business locally.

- Website: (Search “City of Rancho Cucamonga Economic Development”)

- Rancho Cucamonga Chamber of Commerce: Offers networking opportunities, business advocacy, local market insights, and resources for businesses operating within the city. Valuable for connecting with the local business community.

- Website: (Search “Rancho Cucamonga Chamber of Commerce”)

- Inland Empire Small Business Development Center (SBDC): Provides free, confidential business consulting and low-cost training services to entrepreneurs and small businesses throughout the region, including Rancho Cucamonga. Excellent resource for business planning, financial projections, and loan application assistance.

- Website: (Search “Inland Empire SBDC”)

- SCORE Inland Empire: A non-profit association offering free mentorship from experienced business professionals. Volunteers can guide startups and existing businesses on strategy, finance, marketing, and operations.

- Website: (Search “SCORE Inland Empire”)

- California Governor’s Office of Business and Economic Development (GO-Biz): Offers information on statewide business incentives, programs, and resources that may benefit businesses and investors in Rancho Cucamonga and across California.

- Website: (Search “California GO-Biz”)

- Inland Empire Economic Partnership (IEEP): Provides regional economic data, research, and advocacy, offering valuable insights into the broader economic trends affecting Rancho Cucamonga and the Inland Empire – useful for investor due diligence.

- Website: (Search “Inland Empire Economic Partnership”)

These resources can provide valuable data, connections, and support systems for investors evaluating opportunities and for businesses seeking to thrive in the Rancho Cucamonga area, potentially strengthening their case when applying for a small business loan.

Partnering for Success: Why Consider GHC Funding?

Choosing the right lending partner is as critical as choosing the right type of small business loan. When your funding needs involve commercial real estate or require a lender who understands the complexities of business finance, working with a specialist can make a significant difference.

GHC Funding focuses on providing tailored financing solutions, including:

- Commercial Real Estate Loans: Expertise in financing for property acquisition, development, and refinancing.

- Business Loans: Offering various business funding options to meet diverse needs like working capital, expansion, and equipment.

Partnering with a firm like GHC Funding means access to experienced professionals who can help navigate the application process and structure a loan that aligns with your business goals. Explore their loan programs to see how they can support your venture.

Conclusion: Taking the Next Step Towards Funding Your Vision

Securing a small business loan is a significant step that can propel your business forward, enabling growth, stability, and the realization of your entrepreneurial vision. While the process requires careful preparation and understanding, it’s far from insurmountable.

By identifying your specific funding needs, understanding the different types of loans available, diligently preparing your documentation, and knowing what lenders look for, you dramatically increase your chances of success. Remember to explore all options, from traditional bank loans and SBA programs to specialized financing like that offered by GHC Funding, especially for commercial real estate and tailored business capital needs.

Whether you’re just starting, planning a major expansion, or navigating the day-to-day financial demands of running a business, the right small business loan can be the key that unlocks your potential. Take the time to research, prepare, and choose the financing solution that best fits your unique circumstances. Your business’s future may depend on it.

Ready to explore your small business loan options? Contact GHC Funding today to discuss your financing needs. Visit GHC Funding

GHC Funding: Your Ultimate Guide to SBA Small Business Loans in Rancho Cucamonga, California for 2024

Contact Information:

- GHC Funding

- Phone: 833-572-4327

- Email: sales@ghcfunding.com

- Website: www.ghcfunding.com

Disclaimer: This blog post is for informational purposes only and does not constitute financial advice. Always consult with a financial advisor before making any financing decisions.

Introduction

Rancho Cucamonga, California, is a thriving hub for small businesses, offering a unique blend of suburban charm and economic opportunities. Nestled in San Bernardino County, this city has experienced rapid growth, attracting entrepreneurs and small business owners looking to capitalize on its strategic location and supportive business environment. Whether you’re starting a new venture or looking to expand your existing business, Rancho Cucamonga offers a wealth of opportunities. However, securing the right financing is crucial to achieving your business goals.

GHC Funding is here to help small business owners in Rancho Cucamonga navigate the complex world of business financing. As a commercial loan broker, not a bank, GHC Funding provides tailored financing solutions without charging points or fees. In this comprehensive guide, we’ll explore the various financing options available to small businesses in Rancho Cucamonga, with a focus on optimizing for SBA Small Business Loans.

Table of Contents

- Rancho Cucamonga: An Overview

- 1.1. Key Facts and Highlights

- 1.2. Economic Landscape and Business Environment

- 1.3. Top 5 Zip Codes in Rancho Cucamonga

- GHC Funding Services

- 2.1. SBA Loans

- 2.2. Term Loans

- 2.3. Working Capital Loans

- 2.4. Equipment Financing

- 2.5. Business Line of Credit

- 2.6. Commercial Real Estate (CRE) Loans

- Why Choose GHC Funding?

- 3.1. GHC Funding vs. Traditional Banks

- 3.2. No Points or Fees

- 3.3. Customized Loan Solutions

- Client Success Stories

- 4.1. Case Study 1: Retail Business Expansion

- 4.2. Case Study 2: Manufacturing Equipment Financing

- 4.3. Case Study 3: Commercial Real Estate Acquisition

- FAQs on Small Business Lending

- 5.1. What is an SBA Loan?

- 5.2. How Can I Qualify for a Term Loan?

- 5.3. What is the Difference Between a Line of Credit and a Term Loan?

- 5.4. How Can GHC Funding Help with Equipment Financing?

- 5.5. What are the Benefits of Working with a Loan Broker?

- External Resources and Links

- 6.1. Local Government Resources

- 6.2. SBA Resources

- 6.3. Business Support Organizations in Rancho Cucamonga

- Contact GHC Funding

1. Rancho Cucamonga: An Overview

1.1. Key Facts and Highlights

Rancho Cucamonga is a city in San Bernardino County, California, known for its picturesque views of the San Gabriel Mountains and its vibrant economy. Here are some key highlights about Rancho Cucamonga:

- Population: Approximately 180,000 residents.

- Median Household Income: $85,000, well above the national average.

- Business Environment: Rancho Cucamonga has a diverse business environment, with key industries including retail, manufacturing, logistics, and healthcare.

- Education: The city is home to several top-rated schools and a well-educated workforce.

- Transport Links: Convenient access to major highways, including I-10, I-15, and the 210 Freeway, as well as close proximity to Ontario International Airport.

1.2. Economic Landscape and Business Environment

Rancho Cucamonga’s economy is robust and diverse, making it an attractive location for small businesses. The city’s strategic location within the Inland Empire, one of the fastest-growing regions in the United States, provides businesses with access to a large customer base and efficient logistics networks.

The city government actively supports small businesses through various initiatives, including business development programs, tax incentives, and streamlined permitting processes. Additionally, Rancho Cucamonga’s strong community spirit and high quality of life make it an ideal place for entrepreneurs to live, work, and grow their businesses.

1.3. Top 5 Zip Codes in Rancho Cucamonga

- 91730: Central Rancho Cucamonga, home to a mix of residential and commercial properties.

- 91701: Northern Rancho Cucamonga, known for its affluent neighborhoods and proximity to the San Gabriel Mountains.

- 91737: Alta Loma area, offering a suburban feel with easy access to commercial centers.

- 91739: Eastern Rancho Cucamonga, a rapidly growing area with new developments.

- 91786: Southern Rancho Cucamonga, bordering Upland and offering a mix of residential and business areas.

These zip codes represent key areas within Rancho Cucamonga, each offering unique opportunities for small businesses.

2. GHC Funding Services

2.1. SBA Loans

Small Business Administration (SBA) loans are among the most popular financing options for small businesses. These loans are partially guaranteed by the government, making them a low-risk option for lenders and a cost-effective solution for borrowers. GHC Funding specializes in helping businesses secure SBA loans, offering expert guidance throughout the application process.

Key Benefits of SBA Loans:

- Low Interest Rates: SBA loans typically offer lower interest rates compared to traditional business loans.

- Long Repayment Terms: Terms can extend up to 25 years, making monthly payments more manageable.

- Flexible Use: SBA loans can be used for various purposes, including working capital, equipment purchases, and real estate acquisitions.

Types of SBA Loans Offered by GHC Funding:

- 7(a) Loan Program: The most common SBA loan, ideal for working capital, purchasing equipment, or refinancing existing debt.

- 504 Loan Program: Designed for purchasing fixed assets like real estate or machinery.

- Microloans: Smaller loans (up to $50,000) for startups and microbusinesses.

2.2. Term Loans

Term loans provide a lump sum of capital that is repaid over a fixed period, typically ranging from one to five years. GHC Funding offers term loans with competitive rates and flexible terms tailored to the needs of small businesses in Rancho Cucamonga.

Advantages of Term Loans:

- Predictable Payments: Fixed monthly payments make it easier to budget and manage cash flow.

- Quick Access to Capital: Ideal for businesses needing immediate funds for expansion, equipment purchases, or other large expenses.

- Customizable Terms: Loan amounts and repayment periods can be adjusted to suit your business’s financial situation.

2.3. Working Capital Loans

Working capital loans are designed to help businesses cover day-to-day operating expenses, such as payroll, rent, and inventory purchases. These loans are crucial for maintaining smooth operations, especially during periods of low cash flow.

Benefits of Working Capital Loans:

- Short-Term Financing: Quick access to funds to cover immediate expenses.

- Flexible Repayment: Terms can be customized to match your business’s cash flow cycle.

- No Collateral Required: Many working capital loans are unsecured, meaning you don’t need to pledge assets to qualify.

GHC Funding works with businesses to secure working capital loans that meet their specific needs, ensuring they have the financial flexibility to thrive in Rancho Cucamonga’s competitive market.

2.4. Equipment Financing

For businesses that rely on machinery, technology, or other equipment, financing these assets can be a significant challenge. GHC Funding offers equipment financing solutions that allow businesses to acquire the tools they need without draining their cash reserves.

Key Features of Equipment Financing:

- Preserve Cash Flow: Spread the cost of expensive equipment over time, keeping more cash on hand for other business needs.

- Tax Benefits: In many cases, the interest paid on equipment loans can be deducted as a business expense.

- Fast Approval: Equipment financing through GHC Funding can be approved quickly, allowing businesses to purchase essential equipment without delay.

2.5. Business Line of Credit

A business line of credit provides flexible financing that businesses can draw on as needed, making it an excellent tool for managing cash flow, covering unexpected expenses, or taking advantage of growth opportunities.

Advantages of a Business Line of Credit:

- Flexibility: Borrow only what you need, when you need it, and repay it as you go.

- Revolving Credit: Once repaid, the funds become available again for future use.

- No Fixed Payments: Unlike term loans, you only pay interest on the amount you draw, giving you control over your monthly payments.

GHC Funding helps businesses in Rancho Cucamonga secure lines of credit that provide financial flexibility without the rigid terms of traditional loans.

2.6. Commercial Real Estate (CRE) Loans

For businesses looking to purchase, refinance, or renovate commercial properties in Rancho Cucamonga, GHC Funding offers competitive Commercial Real Estate (CRE) loans. These loans are essential for businesses seeking to establish a physical presence or expand their operations.

Benefits of CRE Loans:

- Long-Term Financing: CRE loans typically offer longer repayment terms, reducing the strain on monthly cash flow.

- Competitive Rates: As a commercial loan broker, GHC Funding can secure favorable rates that traditional banks may not offer.

- Customized Solutions: Whether you’re purchasing a new property or refinancing an existing one, GHC Funding provides tailored loan solutions to meet your specific needs.

3. Why Choose GHC Funding?

3.1. GHC Funding vs. Traditional Banks

Choosing the right financing partner is crucial for small businesses. While traditional banks offer a range of loan products, they often come with strict requirements, lengthy approval processes, and hidden fees. GHC Funding, on the other hand, provides a more flexible and personalized approach to business financing.

Key Differences:

- Faster Approval: GHC Funding’s streamlined processes mean you can secure financing quicker than with most banks.

- Flexible Terms: Loans are tailored to your business’s needs, not a one-size-fits-all approach.

- No Hidden Fees: GHC Funding is transparent about costs, with no points or fees added to your loan.

3.3. Customized Loan Solutions

Every business is unique, with its own set of challenges and opportunities. At GHC Funding, we understand that a one-size-fits-all approach doesn’t work when it comes to business financing. That’s why we take the time to understand your business’s specific needs and goals, offering customized loan solutions that align with your vision for growth.

4. Client Success Stories

4.1. Case Study 1: Retail Business Expansion

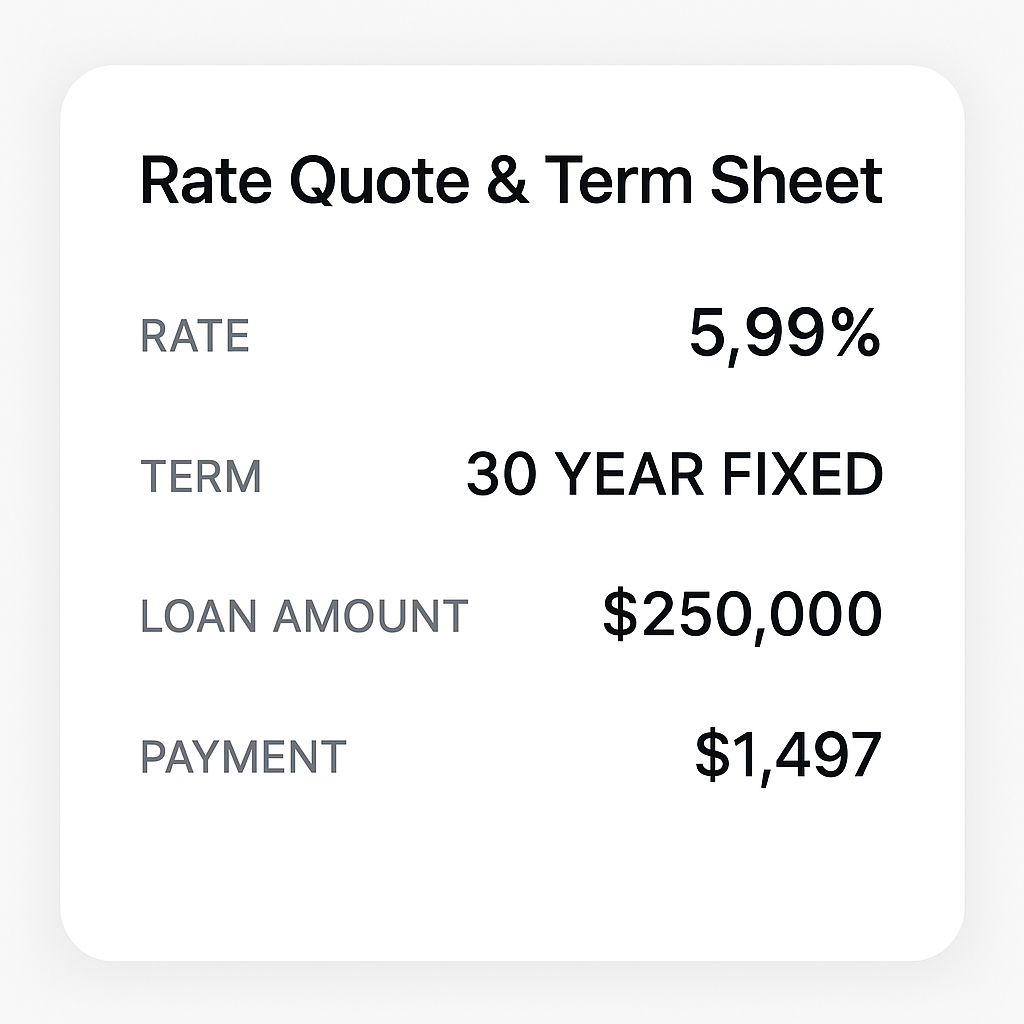

Client: A family-owned retail store in Rancho Cucamonga looking to open a second location.

Challenge: The client needed financing to lease a new storefront, purchase inventory, and hire additional staff.

Solution: GHC Funding secured a $250,000 SBA 7(a) loan, which provided the necessary capital to cover all expansion costs. The flexible repayment terms allowed the business to manage cash flow effectively during the growth phase.

Outcome: The new location opened on schedule, and within the first year, the business saw a 30% increase in revenue.

4.2. Case Study 2: Manufacturing Equipment Financing

Client: A small manufacturing company in Rancho Cucamonga needing to upgrade its production line.

Challenge: The client required financing for new machinery but didn’t want to deplete their cash reserves.

Solution: GHC Funding arranged an equipment financing loan with a 5-year term, allowing the business to spread the cost of the new equipment over time.

Outcome: The new machinery increased production capacity by 50%, enabling the company to take on larger contracts and boost profitability.

4.3. Case Study 3: Commercial Real Estate Acquisition

Client: A professional services firm in Rancho Cucamonga looking to purchase a commercial property.

Challenge: The client wanted to secure a loan with favorable terms to buy their own office space, reducing long-term overhead costs.

Solution: GHC Funding facilitated a Commercial Real Estate (CRE) loan with a 15-year term and competitive interest rate, tailored to the client’s financial situation.

Outcome: The firm successfully purchased the property, reducing monthly expenses by 20% compared to their previous lease.

5. FAQs on Small Business Lending

5.1. What is an SBA Loan?

An SBA loan is a government-backed loan designed to help small businesses access affordable financing. These loans are partially guaranteed by the Small Business Administration, reducing the risk for lenders and making it easier for small businesses to qualify.

5.2. How Can I Qualify for a Term Loan?

To qualify for a term loan, your business will typically need a solid credit history, a strong business plan, and sufficient cash flow to cover loan payments. GHC Funding can help you assess your eligibility and guide you through the application process.

5.3. What is the Difference Between a Line of Credit and a Term Loan?

A term loan provides a lump sum of money that is repaid over a fixed period, while a line of credit allows you to borrow funds as needed, up to a certain limit, and only pay interest on the amount you draw.

5.4. How Can GHC Funding Help with Equipment Financing?

GHC Funding offers equipment financing solutions that allow businesses to acquire essential machinery without depleting cash reserves. We provide flexible terms and fast approval, ensuring you can get the equipment you need when you need it.

5.5. What are the Benefits of Working with a Loan Broker?

Working with a loan broker like GHC Funding gives you access to a wider range of loan products and lenders. We can negotiate better terms on your behalf and provide personalized advice based on your business’s unique needs.

6. External Resources and Links

Local Government Resources:

SBA Resources:

Business Support Organizations in Rancho Cucamonga:

7. Contact GHC Funding

GHC Funding is your trusted partner for small business financing in Rancho Cucamonga, California. Whether you need an SBA loan, equipment financing, or a business line of credit, we’re here to help you achieve your business goals.

Contact Information:

- GHC Funding

- Phone: 833-572-4327

- Email: sales@ghcfunding.com

- Website: www.ghcfunding.com

Disclaimer: This blog post is for informational purposes only and does not constitute financial advice. Always consult with a financial advisor before making any financing decisions.

This comprehensive guide is designed to provide small business owners in Rancho Cucamonga with the information they need to secure the right financing for their needs. By working with GHC Funding, you can access tailored loan solutions that support your business’s growth and success in 2024 and beyond.

Get a No Obligation Quote Today.

Use these trusted resources to grow and manage your small business—then connect with GHC Funding

to explore financing options tailored to your needs.

GHC Funding helps entrepreneurs secure working capital, equipment financing, real estate loans,

and more—start your funding conversation today.

Helpful Small Business Resources