Unlocking Commercial Real Estate Success: Your Guide to Underwriting Pro Forma Software (Colorado Edition)

Get real estate underwriting pro forma software in Colorado NOW! In the dynamic world of commercial real estate (CRE), success hinges on meticulous planning, insightful analysis, and strategic financing. Whether you’re a seasoned developer, a budding investor, or a property manager looking to expand your portfolio, the ability to accurately project a property’s financial performance is paramount. This is where commercial real estate underwriting pro forma software becomes your indispensable ally.

This comprehensive guide will delve into the critical role of pro forma software in CRE underwriting, exploring its essential features, how lenders leverage it, and key considerations for securing financing. We’ll also pay special attention to the vibrant Colorado commercial real estate market, providing localized insights and highlighting how a trusted lender like GHC Funding can be a vital partner in your ventures.

In this article:

Need capital? GHC Funding offers flexible funding solutions to support your business growth or real estate projects. Discover fast, reliable financing options today!

⚡ Key Flexible Funding Options:

GHC Funding everages financing types that prioritize asset value and cash flow over lengthy financial history checks:

DSCR Rental Loan

- No tax returns required

- Qualify using rental income (DSCR-based)

- Fast closings ~3–4 weeks

SBA 7(a) Loan

- Lower down payments vs banks

- Long amortization improves cash flow

- Good if your business occupies 51%+

Bridge Loan

- Close quickly — move on opportunities

- Flexible underwriting

- Great for value-add or transitional assets

SBA 504 Loan

- Low fixed rates through CDC portion

- Great for construction, expansion, fixed assets

- Often lower down payment than bank loans

🌐 Learn More

For details on GHC Funding's specific products and to start an application, please visit our homepage:

- The Foundation of Foresight: What is Commercial Real Estate Underwriting Pro Forma Software?

- The Lender's Lens: How Commercial Lenders Underwrite with Your Pro Forma

- Navigating Commercial Loan Rates and Requirements in Today's Market

- GHC Funding: Your Partner in Commercial Real Estate Financing

- Colorado's Commercial Real Estate Landscape: A Focus for Investors

- Essential External Resources for Colorado Investors:

- Conclusion

The Foundation of Foresight: What is Commercial Real Estate Underwriting Pro Forma Software?

At its core, a pro forma is a financial projection for a real estate asset, estimating its future income, expenses, and cash flow over a specific period—often 5, 10, or even 20 years. It’s a forward-looking income statement and cash flow statement for a property, designed to assess its potential profitability and value.

Commercial real estate underwriting pro forma software is the digital powerhouse that automates and streamlines this complex projection process. Moving beyond traditional spreadsheets, these sophisticated tools enable investors and developers to build robust financial models, run countless scenarios, and generate comprehensive reports with unparalleled speed and accuracy.

Essential Features That Elevate Your Analysis:

A truly effective pro forma software solution offers a suite of features designed to enhance every stage of your underwriting process:

- Detailed Property Analysis & Financial Modeling: This is the heart of the software. It allows you to input granular data related to:

- Revenue Streams: Base rental income, absorption and turnover vacancy, concessions, expense reimbursements, percentage rent (for retail), and other income. You can model rent growth, lease expirations, market leasing assumptions, and renewal probabilities.

- Operating Expenses: Property taxes, insurance, utilities, repairs and maintenance, property management fees, general and administrative expenses.1 The software often allows for expense reimbursements to be accounted for.

- Capital Costs (CapEx, TIs, LCs): Capital expenditures (CapEx) for major repairs or upgrades, tenant improvements (TIs) for new leases, and leasing commissions (LCs) paid to brokers.

- Debt Service: Integrates loan terms (interest rates, amortization, loan amount) to calculate annual debt service.

- Exit Scenarios: Projects the potential sale price of the property at the end of the holding period, often based on a terminal capitalization rate.

- Scenario Modeling & Sensitivity Analysis: One of the most powerful features. Good software allows you to effortlessly create multiple scenarios (e.g., optimistic, base, pessimistic) by adjusting key variables like occupancy rates, rent growth, interest rates, or exit cap rates. This “what-if” analysis is crucial for understanding risk and potential returns under various market conditions. It helps you identify the assumptions that have the most significant impact on your project’s viability.

- Property Comparison: For investors evaluating multiple acquisition opportunities, the ability to compare pro formas side-by-side or analyze a portfolio of properties is invaluable. This feature can highlight the best investment opportunities based on your specific criteria.

- Robust Reporting & Visualization: The software should generate professional, customizable reports including:

- Pro forma income statements and cash flow projections.

- Rent rolls and market leasing projections.

- Construction loan budgets.

- Key performance indicators (KPIs) like Net Operating Income (NOI), Debt Service Coverage Ratio (DSCR), Loan-to-Value (LTV), Internal Rate of Return (IRR), Cash-on-Cash Return, and Capitalization Rate (Cap Rate).

- Visual dashboards with charts and graphs that clearly communicate financial performance and risk.

- Error Reduction & Efficiency: By automating calculations and data aggregation, pro forma software significantly reduces the risk of human error inherent in manual spreadsheet work. This saves countless hours and enhances the reliability of your projections.

- Collaboration & Sharing: Features that allow multiple team members to work on or review pro formas, with version control and easy sharing capabilities, are essential for larger teams and for presenting to lenders or partners.

The Lender’s Lens: How Commercial Lenders Underwrite with Your Pro Forma

For commercial lenders, your pro forma isn’t just a document; it’s a window into the future performance and risk profile of your proposed investment. They don’t just glance at it; they scrutinize it, often building their own pro forma based on their conservative underwriting standards.

Here’s how lenders primarily use and evaluate your pro forma for underwriting:

- Net Operating Income (NOI): This is the bedrock. Lenders meticulously verify your projected gross operating income (rent, other income) and subtract operating expenses. They will often apply conservative assumptions for vacancy rates and operating expenses, sometimes adjusting your figures to reflect their own market insights or historical averages. A strong, stable, and realistically projected NOI is fundamental.

- Debt Service Coverage Ratio (DSCR): This is paramount. The DSCR (NOI / Annual Debt Service) indicates a property’s ability to generate enough income to cover its loan payments. Lenders typically look for a DSCR above a certain threshold, often 1.20x to 1.30x or higher, depending on the property type, market, and loan product. A higher DSCR provides a larger cushion against unexpected expenses or income fluctuations. Our DSCR Loan Calculator can help you quickly assess this crucial metric.

- Loan-to-Value (LTV): This ratio (Loan Amount / Property Value) assesses the level of leverage on the asset. Lenders typically have maximum LTV thresholds, often ranging from 65% to 80% for commercial properties, with lower LTVs signifying less risk for the lender. The property’s appraised value, which the lender commissions, will heavily influence this.

- Debt Yield: An increasingly important metric, especially for CMBS and some non-recourse loans. Debt yield (NOI / Loan Amount) measures the lender’s return on investment if they were to foreclose on the property. It provides a quick way for lenders to assess risk, independent of the interest rate or amortization. Lenders often seek debt yields of 8% to 10% or higher.

- Market Analysis: Lenders validate your pro forma’s assumptions against current market conditions, vacancy rates, rent trends, and economic forecasts for the specific submarket. They assess the supply and demand dynamics, comparable sales, and lease data to ensure your projections are grounded in reality. This is particularly vital in diverse markets like those found throughout Colorado.

- Borrower Creditworthiness & Experience: While a strong pro forma focuses on the property, lenders also evaluate the borrower’s financial strength, credit history, and relevant experience in managing similar assets. A well-capitalized borrower with a proven track record can sometimes offset minor deficiencies in a pro forma, especially for value-add or development projects.

Your pro forma software’s ability to generate detailed, transparent, and defensible projections, coupled with robust scenario analysis, directly impacts a lender’s confidence in your project.

Navigating Commercial Loan Rates and Requirements in Today’s Market

Commercial real estate financing is subject to a myriad of factors, including macroeconomic conditions, Federal Reserve policy, inflation, and investor sentiment. While I cannot provide real-time, “as of date” rates (as these fluctuate daily and vary by lender, property type, and borrower profile), we can discuss the current landscape and general requirements.

General Rate Environment (Illustrative Trends – May 2025 Context):

In recent times, we’ve observed a period of interest rate adjustments by the Federal Reserve aimed at managing inflation. While there have been discussions of potential easing cycles, the commercial real estate lending environment remains sensitive to these shifts.

- Prime Rate: Typically used for variable-rate loans, the Prime Rate closely tracks the Federal Funds Rate. It serves as a benchmark for many commercial lines of credit and short-term loans.

- SOFR (Secured Overnight Financing Rate): Replacing LIBOR as the primary benchmark for floating-rate commercial loans, SOFR is also influenced by Federal Reserve actions and interbank lending conditions.

- Fixed vs. Variable: Borrowers often weigh fixed-rate loans (offering payment predictability, often tied to U.S. Treasury yields plus a spread) against variable-rate loans (which may start lower but carry interest rate risk, typically tied to Prime or SOFR).

- Property Type Influence: Rates can vary significantly by asset class. For instance, stable multifamily or industrial properties might command more favorable terms due to lower perceived risk compared to speculative office or retail developments in evolving markets.

- Lender-Specific Pricing: Each lender, including agencies like Fannie Mae and Freddie Mac (for multifamily), and government-backed programs like SBA, will have their own pricing models, spreads, and fees.

Common Commercial Loan Requirements:

Securing commercial real estate financing involves meeting several key criteria:

- Strong Financials (Borrower & Property):

- Personal and Business Credit Scores: Lenders will examine both. A strong personal credit score (often 680+) and a solid business credit history are crucial.

- Cash Flow: Demonstrated ability to cover debt service, both from the property’s NOI and the borrower’s global cash flow.

- Liquidity & Net Worth: Lenders want to see sufficient liquid reserves to cover potential operating shortfalls and robust overall net worth.

- Borrower Experience: Proven experience in managing similar commercial properties or successful business ventures.

- Property Specifics:

- Property Type & Condition: The asset must align with the lender’s comfort level and portfolio strategy. It must be in good condition or have a clear plan for improvements.

- Location: Desirable location with strong market fundamentals.

- Appraisal: An independent appraisal confirming the property’s value.

- Environmental Reports: Phase I environmental site assessments are typically required.

- Zoning & Permitting: Ensuring the property’s use and any planned development align with local zoning and permits.

- Loan Specifics:

- Down Payment/Equity Contribution: Commercial loans typically require a significant equity injection, often 20-35% or more of the project cost.

- Loan-to-Value (LTV) & Debt Service Coverage Ratio (DSCR): Meeting the lender’s specific thresholds for these critical metrics.

- Business Plan (for new developments/acquisitions): A detailed and compelling business plan outlining the project’s strategy, market analysis, and financial projections.

GHC Funding: Your Partner in Commercial Real Estate Financing

Navigating the complexities of commercial real estate financing requires a lender that understands your vision and can provide tailored solutions. GHC Funding specializes in providing both CRE loans and business loans, offering a comprehensive suite of financing options designed to support your commercial real estate ventures.

Whether you’re looking for acquisition financing for an income-producing property, construction loans for a new development, or refinancing options for an existing asset, GHC Funding offers competitive terms and a streamlined process. Their expertise spans various property types, and they are committed to helping you achieve your investment goals. Explore their offerings and get started on your next project by visiting www.ghcfunding.com.

Colorado’s Commercial Real Estate Landscape: A Focus for Investors

Colorado boasts a vibrant and diverse commercial real estate market, driven by robust economic growth, a strong job market, and continued population migration. For investors utilizing “commercial real estate underwriting pro forma software,” understanding these local nuances is key to optimizing projections and identifying prime opportunities.

Key Commercial Real Estate Markets and Characteristics in Colorado:

- Denver Metro Area: The economic engine of the state.

- Downtown Denver / Central Business District (CBD) (e.g., 80202, 80203): Known for skyscrapers, corporate HQs, and a growing residential population. While the office market has faced challenges due to remote work shifts, there’s a “flight to quality” with demand for modern, amenity-rich spaces. New developments and redevelopations in areas like the Union Station neighborhood continue to attract activity.

- RiNo (River North) Arts District (e.g., 80205): A prime example of urban revitalization, transforming industrial spaces into trendy offices, creative studios, retail, and multifamily units. High demand for flex and creative office spaces.

- Denver Tech Center (DTC) (e.g., 80111, 80112): A sprawling suburban commercial hub offering a mix of office, retail, and hospitality. Remains a strong employment center for south Denver suburbs like Greenwood Village and Centennial.

- Aurora (e.g., 80010, 80011): Colorado’s third-largest city, offering affordable alternatives to Denver, with significant growth in industrial, retail, and healthcare sectors. Proximity to Denver International Airport (DIA) fuels logistics and distribution.

- Lakewood (e.g., 80214, 80226): A diverse suburban market with a mix of retail, office, and multifamily, benefitting from its location west of Denver and access to the mountains.

- Industrial Sector: Strong demand across the metro for warehouses, distribution centers, and flex industrial, driven by e-commerce and logistics. Submarkets near major highways (I-70, I-25) and DIA (like those in Commerce City or near Brighton) are particularly active.

- Multifamily: Consistent demand due to population growth, though some submarkets are experiencing new supply, leading to increased concessions in Class A properties.

- Colorado Springs (e.g., 80903, 80907, 80909): A rising star, consistently ranked among top housing markets.

- Strong Economy: Driven by military installations (Peterson Space Force Base, Fort Carson, Air Force Academy), aerospace, and tech sectors.

- Affordability: Offers a more affordable entry point than Denver, attracting both residents and businesses.

- Growth: Significant new construction and population growth support demand for all commercial property types, especially retail and light industrial.

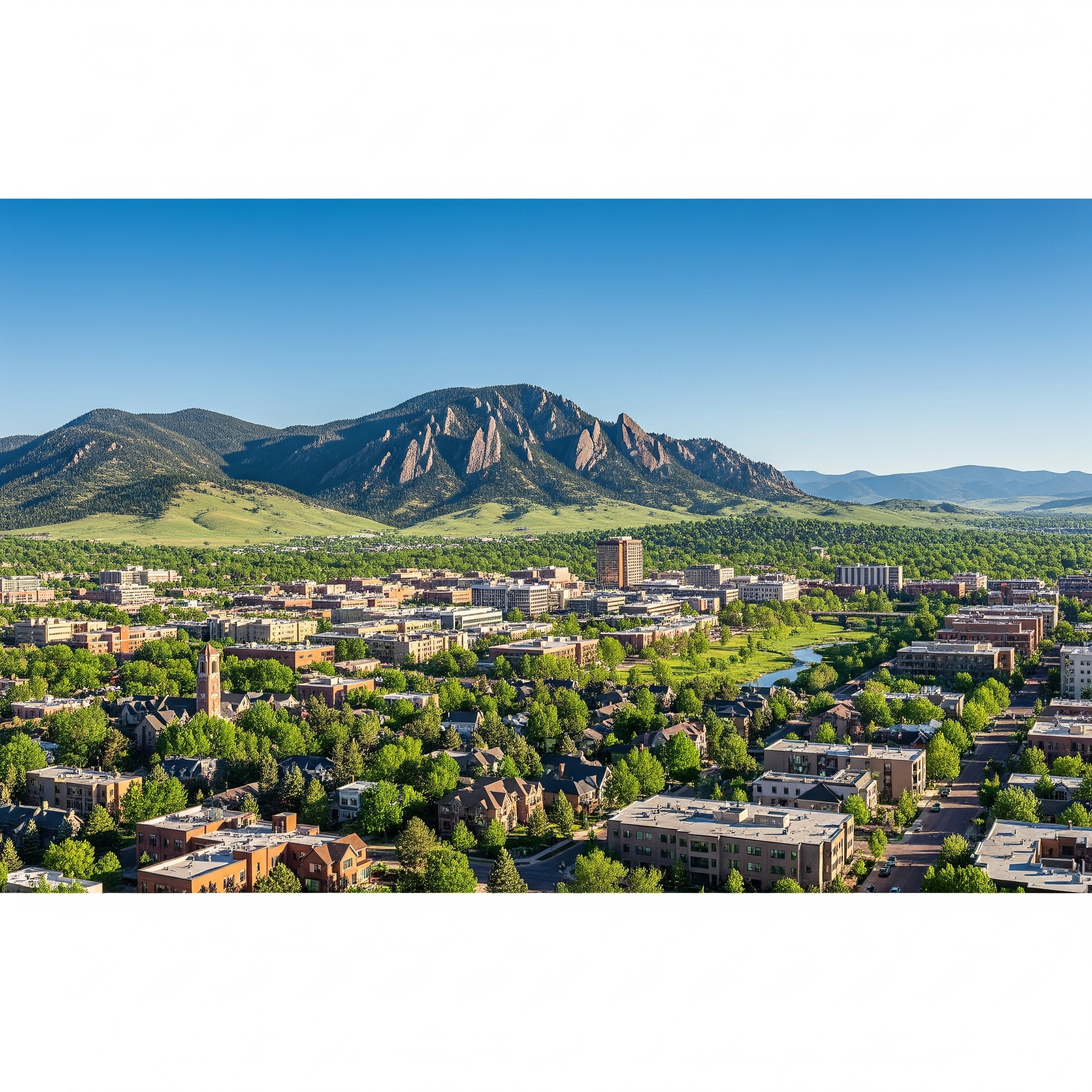

- Boulder (e.g., 80302, 80303): A hub for tech, biotech, and research.

- Innovation Economy: Home to numerous startups and major tech companies, alongside the University of Colorado Boulder, driving demand for office, lab, and specialized retail spaces.

- High Demand, Limited Supply: Due to geographic constraints and strict zoning, commercial real estate here commands premium prices and low vacancy rates, making strong pro forma projections even more critical.

- Fort Collins (e.g., 80521, 80525): Northern Colorado’s economic hub.

- University Town: Home to Colorado State University, creating steady demand for student housing, retail, and supporting services.

- Diverse Economy: Strong sectors in advanced manufacturing, clean energy, and ag-tech.

- Quality of Life: Attracts residents and businesses seeking a balance of urban amenities and outdoor recreation.

- Pueblo (e.g., 81001, 81007): An emerging market offering affordability and growth potential.

- Lower Entry Point: Significantly more affordable than the Front Range cities, attracting investors seeking higher cap rates and appreciation potential.

- Industrial Growth: Developing as a logistics and manufacturing hub.

- Grand Junction (e.g., 81501, 81505): Western Slope’s largest city.

- Regional Hub: Serves as a commercial and healthcare hub for western Colorado and eastern Utah.

- Affordability & Outdoor Tourism: Attracts residents seeking a lower cost of living and outdoor recreation, supporting retail, hospitality, and industrial sectors.

- Greeley (e.g., 80631, 80634): Part of the rapidly growing Northern Colorado region.

- Agricultural & Energy Base: Strong traditional economic drivers with diversification into manufacturing and healthcare.

- Affordability: Offers relative affordability and consistent growth, especially in residential and supporting commercial properties.

Geo-Targeting and Local Market Analysis:

When utilizing your commercial real estate underwriting pro forma software, remember to integrate local market data for maximum accuracy and SEO benefit. This means:

- Drilling Down to Submarkets: Don’t just analyze “Denver”; look at Downtown, LoDo, RiNo, Cherry Creek, DTC, Broomfield, or specific zip codes (e.g., 80202 for Downtown, 80111 for DTC, 80205 for RiNo) within the metro area. Each has unique supply/demand dynamics, rental rates, and vacancy trends.

- Local Economic Indicators: Incorporate data on local job growth, population changes, average household incomes, and industry-specific trends that impact demand for various property types.

- Comparable Properties: Ensure your pro forma’s assumptions for rents, expenses, and vacancy rates are benchmarked against truly comparable properties within the same submarket or neighborhood (e.g., specific blocks in LoDo, the industrial parks near E-470, neighborhood retail centers in Highlands Ranch).

- Zoning and Regulations: Understand specific zoning laws, development moratoriums, or incentives that apply to your target property’s precise location.

Essential External Resources for Colorado Investors:

To complement your pro forma software and local market analysis, here are types of external resources that can be immensely helpful for commercial real estate investors in Colorado. You should always verify these links for the most current information:

- Colorado Office of Economic Development and International Trade (OEDIT): Provides insights into statewide economic trends, business incentives, and programs like Opportunity Zones (e.g., Denver’s Opportunity Zones in areas like Five Points or West Colfax, or specific zones in Pueblo or Colorado Springs). Their website can offer economic data and an investment database.

- Colorado Real Estate Commission: Offers licensing information and regulatory guidelines for real estate professionals in the state.

- Local Economic Development Agencies: Key resources for detailed local data, zoning information, and development incentives. Examples include:

- Denver Economic Development & Opportunity (DEDO)

- Colorado Springs Economic Development Corporation (EDC)

- Boulder Economic Council

- Northern Colorado Economic Development Corporation (NCEDC) for Fort Collins and Greeley area.

- Local Commercial Real Estate Brokerages: Major national and regional brokerages (e.g., CBRE, JLL, Cushman & Wakefield, NAI Shames Makovsky) publish quarterly market reports with detailed statistics on vacancy, rental rates, and absorption for various property types across Colorado’s key markets.

- Commercial Real Estate Investment Associations (REIAs): Local groups often host networking events, educational seminars, and provide access to localized market insights and potential deal flow. Search for “Colorado Commercial Real Estate Investment Association” or similar groups in Denver, Colorado Springs, or Boulder.

- County Assessors’ Websites: For property specific tax information and sometimes sales data.

- U.S. Census Bureau & Bureau of Labor Statistics: For macro-level demographic and employment data relevant to Colorado.

Conclusion

In the competitive landscape of commercial real estate, relying on guesswork is a recipe for disaster. Commercial real estate underwriting pro forma software is no longer a luxury but a fundamental tool for anyone serious about making informed investment decisions. It empowers you to analyze opportunities with precision, mitigate risks through robust scenario planning, and present compelling proposals to lenders.

For those looking to invest in the thriving markets of Colorado—from the dynamic urban core of Denver (including neighborhoods like LoDo and RiNo) and its expanding suburbs like Aurora and Lakewood, to the growing cities of Colorado Springs and Fort Collins, and the emerging opportunities in Pueblo or Grand Junction—accurate, localized financial projections are paramount.

When you’re ready to turn your meticulously crafted pro forma into a tangible asset, remember to connect with a reliable financing partner. GHC Funding stands ready to support your commercial real estate and business loan needs, offering the expertise and resources to help you capitalize on the promising opportunities across Colorado. Visit www.ghcfunding.com to learn more about how they can help bring your next successful project to fruition. Equip yourself with the right software, partner with the right lender, and build your future in commercial real estate on a foundation of foresight and financial clarity.

Get a No Obligation Quote Today.

Use these trusted resources to grow and manage your small business—then connect with GHC Funding

to explore financing options tailored to your needs.

GHC Funding helps entrepreneurs secure working capital, equipment financing, real estate loans,

and more—start your funding conversation today.

Helpful Small Business Resources